It’s one of those terms that has many of us non-techies glazing over, but blockchain offers real benefits that merit wider appreciation.

So – for the uninitiated – what exactly is blockchain? Perhaps it’s best to start by describing what it does. The basic concept of blockchain technology is to bridge the trust gap between people and/or organizations, enabling them to share valuable data stored in multiple computer servers in a secure and tamper-proof way. Once data is recorded, it is very difficult, if not impossible, to change, and this is Blockchain’s core strength.

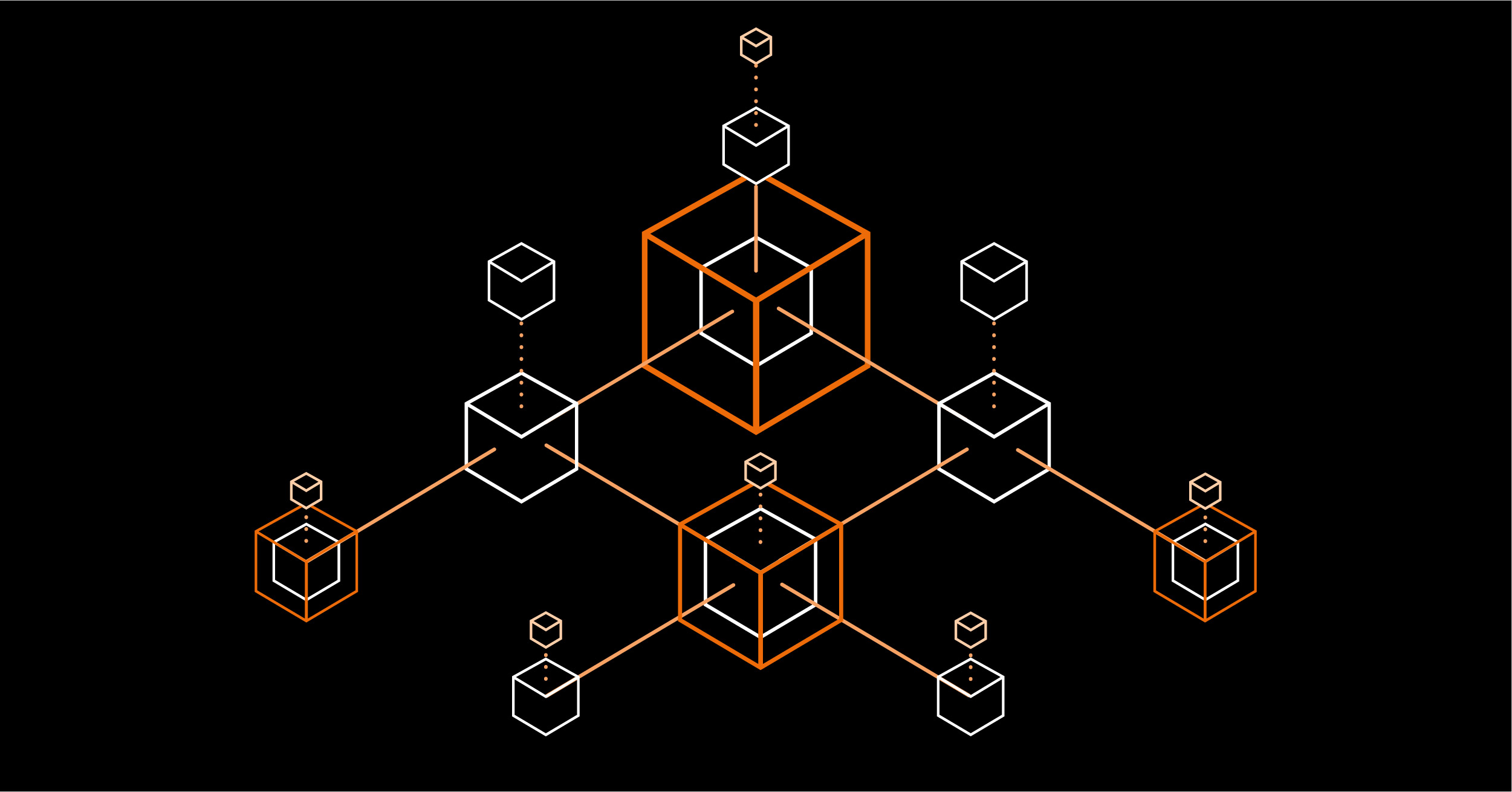

Schematically, blockchain is a chain of information blocks, a data ledger that is distributed, decentralized, and immutable. Every block in the chain has these basic elements: data, time-stamp, hash, and hash of the previous block. Data can comprise information of any type, such as amount, sender, recipient, and address.

Hash is an encrypted alphanumeric identification code that is unique for every block in the openly distributed ledger. Because each block is chained to its predecessor, tampering with the data in an individual block will make all the subsequent blocks invalid. The invalid block will then be replaced by the valid records stored by other devices.

Let’s look at some uses of blockchain…

Sometimes there is confusion between the terms cryptocurrency and blockchain. They are not the same but are interrelated in that cryptocurrencies such as Bitcoin or Ethereum use the blockchain protocol to run on and underpin their security. You can think of the cryptocurrency as the application and blockchain as the operating system. With thousands of cryptocurrencies emerging, blockchain will remain a valuable enabling technology in the financial world.

Blockchain security offers the disruptive prospect of bypassing processing fees imposed by banks and thus lowering transaction costs for consumers. It remains to be seen whether regulatory bodies in different countries will allow this to happen, and with banks themselves investing in blockchain, the picture is still cloudy.

Facilitated by the immensely secure blockchain platform, smart contracts Explanation enable two or more parties to fulfill the terms of a pre-prepared contract using ‘If-This-Then-That’ logic. With each step and obligation rapidly confirmed and verified, it can ease and speed complex or high-value agreements.

Blockchain has application across almost every aspect of retail. Here are just a few examples:

Blockchain allows easy tracking of products through manufacture and supply, warehousing, customs, distribution, retail and after-sale warranty. The result is that the consumer is assured of product authenticity and corporate image is safeguarded. Luxury brands such as Louis Vuitton, Cartier and Prada have partnered with Aura Blockchain Consortium to tackle counterfeit goods

Groupe Renault, Simoldes, Faurecia, Knauf Industries and Coşkunöz came together to develop the XCEED (eXtended Compliance End-to-End Distributed) blockchain project to certify the compliance of all vehicle components, from design to production. This new blockchain solution was developed in association with IBM.

Faulty products batches can be tracked and recalled within a shorter time as all the data in the supply chain is documented. This improves the trust between customer and brand.

In 2018, global transport and logistics specialists, Kuehne+Nagel, adopted blockchain technology to upgrade its VGM (Verified Gross Mass) Portal. Determining the VGM of shipping containers is essential to ensure the safe loading of cargo vessels. The company also uses Vechain’s blockchain technology to ‘smartify’ parcels and assets – especially luxury goods – by furnishing them with a chip containing a private key that registers ownership information on the blockchain.

Brands including Walmart, Carrefour and Amazon use blockchain systems to keep their inventories updated. One of the chief benefits of blockchain inventory management is that it allows accurate forecasting of demand, helping companies to optimize sales and profitability.

Through the

easy and secure identification of individuals, blockchain can improve the

customer experience and encourage loyalty by assisting a smooth transition between

shopping online to shopping in a physical store.

Blockchain has wide application within our own industry:

To summarise, blockchain technology is gaining popularity across many industries but still faces many challenges before it achieves universal adoption. For example, it needs a widely accepted governance and regulatory framework. It also needs to bring all the eco-system players together, not just to achieve better business outcomes but to keep the interests of the consumer in focus.

Privacy of data and associated legislation in some parts of the world is still a concern that must be addressed. A fundamental of blockchain security is that it does not erase data. Consequently, it is important for companies to choose the appropriate type of blockchain for their organizational and legislative environment.

While it will take time for blockchain to mature, it continues to show great promise, and we at CDI World look forward to applying it whenever and wherever it can benefit our customers, within a number of the services we offer.

Take a look at our other blogs in this series

Talk to us today to find out how we can support you with your exhibit or event, ensuring a memorable and impactful brand experience.

Contact Us